BBQ Nation IPO Analysis by GSN Invest

We have divided this analysis into two parts -

Sector overview and Business model linked novelties (Free)

Path to profit & Key Corporate governance risks (GSN Invest++)

The first part is freely available to anyone to learn and grow. The last part has taken quite some back breaking diligence from our end and is therefore only available to paid GSN Invest++ users. If you're not a GSN Invest++ member, you can join today - Join the pack

You can now also sign up to get free updates on our blog posts here - WhatsApp Updates

Disclaimer: This is not a recommendation to Subscribe/Avoid, but merely an attempt to explain the nitty-gritty of the buffet dining business model. Please conduct your own diligence or consult an investment advisor for your

Sector overview and Business Model novelties

Presence: Barbeque nation operates 153 restaurants (147 in India across 77 cities and 6 internationally across 3 countries). They operate in the casual dining sub-segment in the restaurant industry, providing better ambience and experience vs quick service restaurants (QSRs) and better affordability vs fine dines (FDRs).

Market potential: The organized restaurant chain market in India, which stood at 39,800cr in FY20 (9.8% of total Indian food service market), and is expected to grow to 96600cr by FY21 (14.8% of the total market) after a contraction to 22900cr in FY21 due to COVID according to the Technopak analysis on the sector. Of this casual dining chains are expected to grow from 13400cr in FY20 to 30200cr in FY25, growing at a 18% CAGR.

Geographic potential: Chain CDRs are increasingly growing in mini metro and tier 1/2 cities. These outlets are typically smaller (~5250 sq ft in metros, 4750 sq feet in tier 1 cities, and 3750 sq ft in tier 2 cities) and therefore cheaper to set up and run while offering great potential to tap into latent demand. The % contribution of non mega metros has grown from 57% to 69% over the last 5 years, a trend which looks likely to continue.

Consumption mix: While food consists of a majority of the sales (74% vs 19% for beverages and 7% for desserts), beverages which have a much lower cost base drive margins. Buffet QSRs are increasingly excluding the beverage from the buffet cost - and selling the beverages at a significant mark-up.

Channel mix: Even prior to the pandemic, people were increasingly preferring eating at home. Dine in as % of total sales dropped sharply from 60% in FY14 to 54% in FY20. While buffet based restaurants including BBQ Nation have hopped on to the delivery platforms via meal packs, the trend is likely to hurt a business where the primarily value proposition is to walk in and eat all you want.

Competition: The food service space was, and shall continue to be extremely fragmented and competitive, with constant pressure from the unorganized sector, standalone hotels, and other domestic and international chains.

The perishable inventory problem: Airlines, hotels, hospitals and restaurants all suffer from one major problem that make most of them terrible investments. Their inventory is perishable - if a restaurant is empty on a Wednesday afternoon, that time is lost for ever. If there is a sudden surge in demand on a Saturday evening, there are only so many customers you can seat - and you'll therefore lose sales. The problem then becomes maximizing utilization, in a competitive market, with limited differentiation - and that is almost always a race to the bottom. Therefore, barring firms with exceptional execution (Jubilant, Indigo, et al), it becomes extremely tough for firms in these sectors, and consequently investors in these firms to generate sufficient returns.

With the sectoral context broadly understood, lets understand the specifics of BBQ Nations economics. How much does it take them to set up a restaurant, what edge do they have in one of the most challenging factors for a restaurant - driving occupancy, and the thousand crore question - whether a path to profit exists.

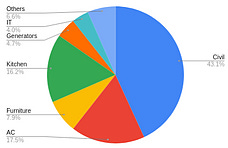

Set up Cost: It takes the firm an approximate 2.1cr to open a new restaurant. Most of the set up cost is in civil amenities, air conditioning, furniture and kitchen equipment. They have been adding close to 20 new restaurants every year (13 in FY17, 23 in FY18, 24 in FY19 and 21 in FY20)

The BBQ Nation Advantage: As we had covered earlier, maintaining occupancy is a key challenge for restaurants. Barbeque nation's fixed price food model, with a lower price on weekdays vs weekends helps even out the utilization on days where it typically would not have been high. This is reflected in the higher weekday sales (53.4% of sales come on weekdays) and higher lunch sales (44.4% from lunch sales). The fixed cost format makes the venue an attractive location for budget outings, that are common in most corporate offices, aiding the weekday and lunch sales.

The path to profit - Growth in users and ASP, difference in profitability between new and mature restaurants and breakdown and trends in each profit item. Read more by joining GSN Invest++ today.

Key Corporate Governance risks - Numerous risks including outstanding litigation, proceedings against promoters, reported and unreported contingent liabilities, suspicious RPTs with a subsidiary and more. Read more by joining GSN Invest++ today.