Garware Technical fibers - Corporate governance red flags

Last two days to register for the November batch of GSN Invest++ Register now to avail lowest subscription rates - Join

Disclaimer - This is an educational exercise meant to teach poeple about potential corporate governance red flags. This is NOT an investment recommendation. Please do your own diligence or consult a investment advisor before taking any investment decision.

We had flagged red flags around management pay and board independence in our piece on La Opala, In this piece we use Garware as an example to highlight potential issues around other income, direct and indirect promoter compensation, and related party transactions.

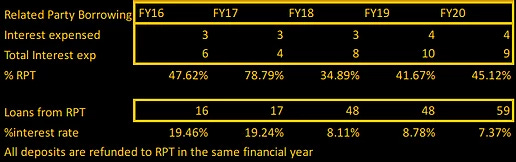

Related party transaction - Why does a company with 380cr of CC&E borrow at 8% from related parties? You don't need a capital allocation class to know that if you have 380cr on your balance sheet earning 6%, it probably doesn't make sense to borrow at significantly higher rates. Garware technical fibers has 104cr as cash and bank deposits and another 280cr in debt funds (more on this later!). Yet the firm routinely borrows from promoters and related parties. It uses this route to pay related parties close to 4cr in interest expense every year - infact half of its interest expense every year is paid to Related parties. These rates used to be extremely healthy earlier and have moderated to the 7-9% range over the last 3 years. All deposits returned in the same year with a healthy 8% interest. Here's the data from the last 5 years.

Promoter pay: Direct & Indirect: Should shareholders pay the promoters 7lakhs/month for his house rent in addition to 7%+ of PAT?

It is second nature for promoters to take healthy salaries and commissions, actively trying to stretch the limits of the 10% PAT. Promoters at Garware have also been fairly liberal with pay, paying themselves ~7% of PAT every year. With the allowances, management pay is close to 9% of PAT - with a one time drop in the current financial year. (Note that this is based on a stretched PAT - so the %of actual PAT will be a lot higher, but more on that in the next segment.)

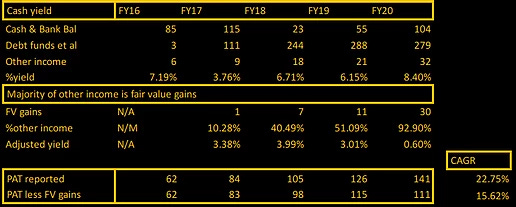

PAT is growing at 23%, but is it really? The exponential fair value adjustment trend?

One statistic that almost everyone who pushes this stock will push is the 23% growth in PAT over the last 5 year. But the PAT is a very fragile number, easily manipulated. Remember the ~280cr the firm has on its books invested largely in debt funds. The firms adjusts that number for changes in fair value of the asset. These changes flow directly to the P&L account through other income, and trickle down from there to the bottom line. What is interesting is not this, but the trend in the FV gains - 1cr, 7cr, 11cr,30cr over the last four years. FV gains have risen from being 10% of other income to 93% of other income. So sharp has been their rise that FV gains now constitute close to 21% of PAT. The 22.75% PAT growth, comes down to a modest 15.6% when adjusted for the FV gains.

Here's the data on that.

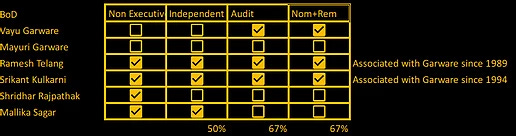

Are key independent directors still independent after 25 years with the firm?

With all this, one would want to see some strong members in the board to flag anything might be appropriate. The firms attempts to check the boxes here with a 50% independent board, and 67% independence on the audit and nomination committees - until you look deeper. The firm has the same two independent directors on both its Audit and Nomination committees, along with the Promoter. Independent directors who are management favourites always get our attention, so we dug deeper. Interestingly both of these directors have been associated with the Garware group for the better part of 25 years. Does this compromise independence? - that's for the shareholders to decide.

[*] All data used in the article is from the firm's website, annual reports, and regulatory filings.

Want to understand 70 market leading firms with a deep dive on quality, corporate governance, growth and longevity? We've got you covered - GSN Invest++