MTAR Technology IPO Analysis by GSN Invest

Disclaimer - This is not an investment recommendation to subscribe/avoid, but merely an attempt to explain a firm and an industry to our users. Please consult your investment advisor or conduct your own diligence before investing.

A) Business context

A different type of B2B: The business to business segment is generally a tough space to compete in, with the client having significant leverage, causing suppliers to compete on price in a vicious negative spiral. There are however exceptions to the norm, with firms offering differentiated business critical products where there is room to exercise pricing power for the right quality.

The natural moats in precision: MTAR technology operates in the precision engineering space. The sector has quite a few features that increase both the pricing power as well as stickiness of the manufacturer. Firstly the industry has exceptionally low error tolerance with the product expected to perform consistently with minimal deviation over long cycles. The low margin of error not only in machining but also finish and heat treatment presents the first barrier to entry in the industry.

The benefits of low margin of error: The moat becomes stronger for precision components servicing industries where the cost of the project is extremely large and the cost of failure is even larger - nuclear, defense, space being some of them. Typical error tolerance in the industry ranges in a few (5-10) microns (10^-6 m).

B) Levers of growth

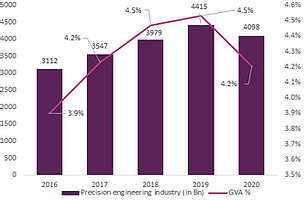

Precision engineering growth: The precision engineering industry in India stands at ₹4,098 bn+ and caters to numerous sectors of national importance including defense, aerospace, nuclear power, space, and railways while also catering to autos, capital goods and wind turbines. It contributes between 3-4% of India’s total manufacturing output, and has been growing at 7.1% vs manufacturing output that grew at 4.9%.

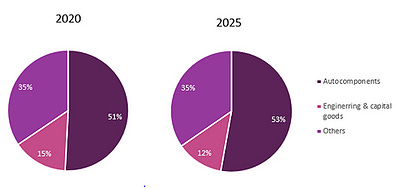

Precision engineering mix: Within precision engineering, auto contributes 50%+ of the output, niche industries like space, nuclear and defense contributing ~33%+ with capital goods contributing the rest. All segments are expected to grow in mid single digits over the next few years.

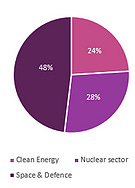

MTAR's four primary areas of expertise - Clean energy, nuclear and space & defense: MTAR Technologies drives most of its revenue from clean energy, nuclear energy, and space and defence.

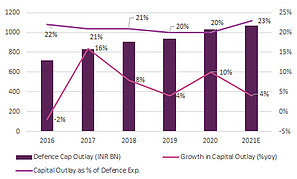

(i) Defence: India has fairly belligerent neighbours both to our west in Pakistan and our north in China, both of whom invest heavily in defense. It becomes critical therefore to have a strong defense spend to strengthen our military might - even if it is primarily preventative.

Over the past 9 years, the defense expenditure to GDP multiple has dropped to less than 1 only once in FY16 which was compensated by a surge in expenditure to 2.5x in FY17. On average, the Indian government spends ~1.8% of its GDP on defense. To boost the defense sector, the government has increased the FDI limit from 49% to 74% under the automatic route so foreign players can have majority control of management and operations and 100% with government approval.

(ii) Nuclear: Global nuclear growth is fueled primarily by APAC countries. Currently the share of nuclear power in India’s total generation is 2.9%. The country’s nuclear energy production witnessed 6.94% CAGR over FY2010-19, while electricity generation itself registered 5.22% CAGR. India’s installed nuclear capacity as of 2019 is 6.25 GW and it is expected to rise to approximately 9.75 GW by 2025 growing at a 8% CAGR.

(iii) Space: India’s satellite launch services are highly cost-competitive and reliable,the launch rate success of PSLV is 96%. The satellite manufacturing and launch systems market in India is estimated to reach Rs 46-48bn by FY2025, at a CAGR of 7-8% in FY2021-25 period. In the past Indian space equipment market grew at CARG 9.4% in FY2017-20. MTAR supplied the engine for PSLV-C25 which launched Mars Orbiter

(iv) Clean Energy: Bloom Energy is the largest client of MTAR driving 65%+ of its revenue. The US has seen the largest deployment of fuel cell energy. Yet, the contribution of fuel cell-based electricity is very low in overall electricity generation, at a minuscule 0.014% in 2019. However, the pace of growth is robust at 12% CAGR between 2015-19, to 150 MW expected to reach 200 MW by 2025.

Broad industry tailwinds: Governmental push towards greater domestic production especially in key areas of defence and space, accelerating trend towards import substitution across sectors, and a broader decarbonization and clean energy push are all likely to work favourably for the company.

Margins: High 60%+ gross margins reflective of differentiated niche product offering - Gross margins are shielded in large part from raw material fluctuation given RM supply in space and defence contracts and CPI linked escalations in nuclear contracts. Employee costs form the second largest cost item at ~24% of costs, but the business sees extremely low employee attrition with the average employee staying with the firm for 15 years. The firm continuously works on incorporation process efficiencies and manufacturing line flexibility in order to maximize utilization and drive up margins.

C) Business robustness

Order Book: The firm has a strong order book of ₹336cr that provides revenue visibility. The book has a healthy mix of defence (₹161cr), nuclear (₹93cr) and clean energy (₹80cr).

Stringent Bidding Criterion: The bidding in the precision engineering space is a lot more stringent and quality focused instead of pure price focused driving better pricing power and barriers to entry. Prior experience is critical in securing new projects - which plays to the strengths of MTAR which has a demonstrable track record.

Long standing relationships Marquee clientele: MTAR has a list of marquee clients including the likes of ISRO (30yr+ relationship) and DRDO (40yr+ relationship) which are India's primary space and research agencies, as well as players in the power space including NPCIL (16yr relationship) and Bloom Energy (9yr relationship). Competitive landscape: Oligopolistic landscape with few high quality competitors including the likes of L&T, Godrej, Mahindra defence, and Hindustan Aeronautics.

Concentration: The company drives 64.5% of its revenue from a single international client ( Bloom Energy). The concentration risk has increased over the last 3 years going up from 49.1% to 64.5%. Deterioration of either Bloom's growth prospects, or MTAR's relationship with Bloom can have a material negative impact on the firm.

The high quality of the business, multiple growth levers, and sound moats make it an attractive business proposition. The lack of an alternative to play on some of the themes that MTAR offers exposure to is likely to pique market interest

GSN Invest++ 100 covers detailed analysis on 100 market leading Indian companies, analyzed by an ex J.P. Morgan, ex Goldman Sachs analyst. Join the revolution today! 🔥