Nazara Technologies - IPO Analysis by GSN Invest

Disclaimer: This is not a recommendation to subscribe/avoid but merely an attempt to explain the various models in the gaming industry better. Please conduct your own diligence or consult an investment advisor before taking any investment decision.

Perhaps the first thing you'll hear about Nazara is that Rakesh Jhunjhunwala is a shareholder in the company - and the big bull's name will drive a lot of interest in the stock. It is however important to understand the details of the business you invest in and not simply get swayed by the halo effect a big investor name brings. In this post, we'll attempt to do just that.

A changing business

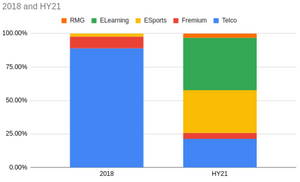

It is educative perhaps to look at the revenue mix of the firm and how it has transformed over the last three years - and the implication of this shift for stability, margins and growth.

The chart gives you a good idea of how the firm is growing as well as the nature of the business today.

Acquisitive of high growth businesses -The firm has invested 300cr+ in acquiring companies over the last 5 years! The firm acquired the Elearning business - Kiddopia ( North America early childhood (2-6yrs) app) in FY20. It aquired the eSportd business - Nodwin Gaming in FY18. Both these businesses while not very profitable have grown tremendously fast and today comprise of more than 71% of the total business.

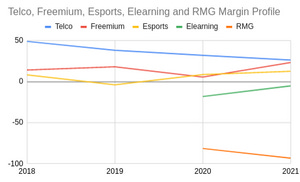

Lower margins - While the traditional businesses - Telco and Freemium gaming have been consistently profitable, the newer businesses have been consistently losing it. And while a path to profit might exist in a few of them - large chunks of the business seem destined to be money losing pits.

So lets dig deeper and understand each of the business lines in greater detail.

1. Early Learning: The segment contributes ~39% of the firm revenue and is the largest segment in the business. A few characteristics of the business stood out the most to us.

Natural churn - Being a business that caters to 2 to 6 year olds, the maximum time you can spend monetizing a customer you acquire is four years. This puts a natural pressure on the amount you can invest into acquiring customers - as well as puts your path to profitability into question. Important to note that this is a natural pull on churn irrespective of how good the business is.

Reporting Quality - The firm is also not extremely transparent in its accounting, reporting cost per trial (CPT) instead of cost per acquisition(CPA). Later in its notes it offers a trial to activation rate of 63.1% for annual and 73.5% for monthly. This takes the cost per acquisition at between 28-32, significantly higher than the reported 20.17 Cost per trial featured prominently in the RHP.

Reported retention : The subscriber retention rate in the business is poor at 25.8%. This means that out of every 1000 customers who join the service at the start of the year, more than 740 leave in the same year. This leads to a vicious cycle of continuously investing to keep more customers coming in through the door - via spending more on marketing and advertising.

Growth: The good news is as the business scales the margins do get better - as your fixed cost base remains broadly constant as you cater to a wider audience, and the firm has been able to keep the cost per trial (not the ideal metric to track, but the only we have) fairly constant. This has led to a gradual improvement in margins.

2. ESports: The segment contributes ~32% of total revenues and is perhaps the best part of the business with both strong revenue growth and improving margins.

Market share & Marquee partners: The firm currently controls 80%+ of the Indian Esports market. It also boasts of a string of marquee partners including Airtel, ESL, Valve Corporation. They have grown these partners from 8 in FY18 to 36 in HY21.

Growth: The growth in esports for the firm has been phenomenal with the business line growing from 3.6cr in FY18 to 84.2 cr in FY20, and 63.7cr in just HY21 alone! The business has also been EBITDA positive.

Sportskeeda: Market leading sports content property in India. The monthly visits on SK have gone up from 2.8cr to 5.9cr between FY18-21, with users spending 1.5x+ time on the website (192minutes vs 129 minutes).

3. Telco: The telco subscription business contributes 21% to the overall revenue. This offering consists of 1000+ android games focussed at the mass-market segment in emerging markets via subscriptions through carrier billing. The business - which was historically very high margin - has been consistently declining both in revenue as well as profitability.

4. Freemium: This business includes free to play sports simulations and children's games including the popular World Cricket Championship game. The business is seeing healthy growth driven by increasingly engaged users (26min/day/user to 41 min/day/user) and an increasing pace of user acquisition (72K/day to 101K/day). While the firm currently has the advantage of the successful WCC franchise that it can monetize - the free gaming market is fragmented and cut throat - which puts the longevity and stability of this business into question. That being said the business has consistently demonstrated its ability to grow - both in revenue and profitability - and is amongst our preferred parts of the business.

5. Real Money gaming: This forms a small part of the overall business at 3%. However it is consistently loss making - and worsening in terms of profitability. Fantasy sports tend to be a winner take all market - as the company with the larger customer base can continue to offer the larger money pool driving more customers to its platform in a positive cycle. There are currently strong players in the market who have established a stronger brand recall and a more dominant market leadership. As the competitors grow larger, the firm will either have to bleed more money to compete (either by investing in the subsidiary or diluting away equity) or exit from the space.

In summary: In the short run the stock seems destined to have a brilliant run on the market driven primarily by one name. Over the long run however - the quality of the business alone will dictate value, and while some parts of the business are extremely compelling (Esports) and others provide some comfort (Telco, Freemium) there are parts of the business that will probably be cash sink-holes for the foreseeable future.

The question then is - is the business appealing enough to warrant a 8x+ revenue multiple, higher than what even robust high-growth international players command?

If this post added value, do show GSN Invest some ❤️

Check out our detailed stock analysis GSN Invest++

Alternately you could support us by donating a small amount