Impact of Revised RBI guidelines on private sector banks

Private banks in India have been on a steady path in growing their share in current accounts, going from 28% in 2015 to ~40% last year. RBI’s latest revised guidelines on opening of current accounts by banks are likely to disrupt that growth path. In today’s post, we explore the kind of impact that private sector banks have to brace for due to this notification.

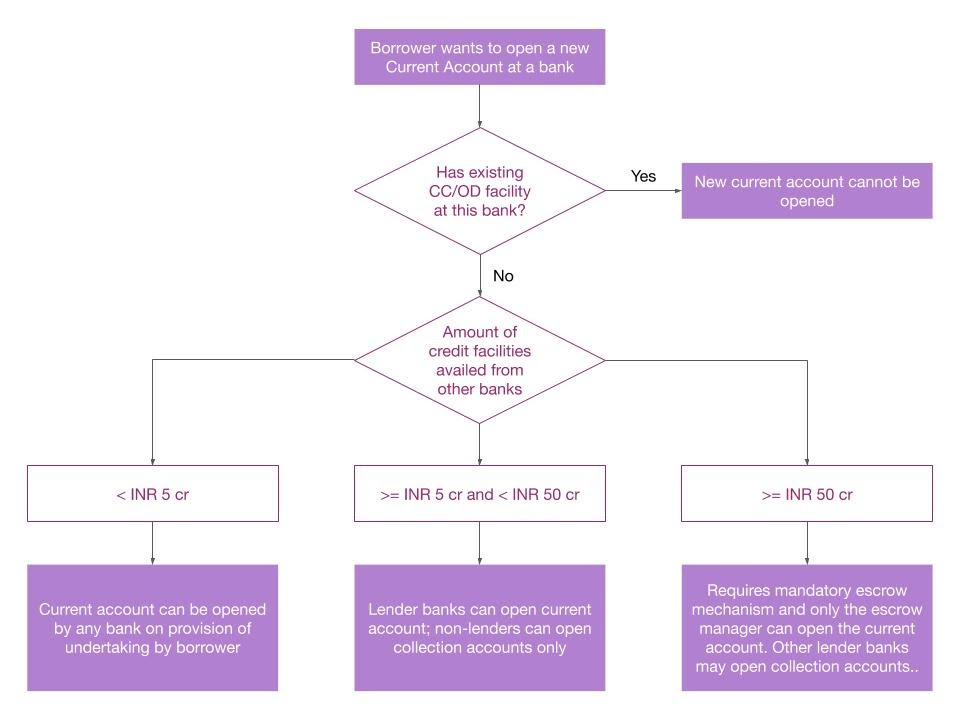

What do the revised guidelines prescribe?

For non-retail borrowers looking to avail cash credit and overdraft (CC/OD) from a certain bank:

For borrowers looking to open new current accounts:

The revised guidelines will require banks to not route withdrawals from term loans through current accounts - instead, the funds will be remitted directly to the borrower’s suppliers. Any expenses incurred towards day-to-day operations will be routed through CC/OD account (if the borrower has one, otherwise a current account can be opened).

Drivers behind the revision

To put it briefly, the revised guidelines are aimed at improving credit discipline and ensuring that lender banks will have more clarity on the cash flows of their borrowers.

Borrowers will no longer be able to have CC/OD and open a current account with two separate banks. This pattern has been quite common as firms could shop for better terms across banks. Many borrowing firms use multiple accounts, often through their subsidiaries, and sometimes opening new accounts for individual projects too. A major fall-out of this ease of ‘shopping’ has manifested as difficulty in monitoring - companies can route payments without providing enough visibility on their financial and operating condition to the lenders.

According to the RBI, the new guidelines will bring a higher level of safeguards as, "the checks and balances put in place in the extant framework, for opening of current accounts, are found to be inadequate”. The system-wide visibility on borrowers will also empower lenders to speed up resolution of stressed borrower accounts. This change comes at a crucial time when covid has dented our NPA reduction trajectory (pl see Japanification - Viral Acharya on the current state of Indian banking).

What does this mean for private sector banks?

The core purpose of the revised guidelines is to ensure that borrowers route their payments to and from a current account with a bank that has the largest exposure to that borrower, instead of having multiple current accounts across banks. This is expected to lead to a trend of current accounts moving towards larger banks. It will also provide support to the consolidation that has been happening in current accounts market share for the last five years. As a result, banks in the private sector, especially the smaller ones will likely take a hit as they will find it difficult to mobilize low-cost deposits through opening current accounts. Fortunately, the banking system as a whole stands to emerge stronger due to this change.

—

Registrations for GSN Invest++ September batch are now open! We analyse 70 of India’s leading public firms for INR 1999 per year (less than INR 30/firm or INR 167/month). You can sign up here: GSN Invest++